The Case for Stronger Digital Controls

Modern accounting systems are powerful, reliable, and designed to automate complexity. They calculate inventory in real time, update reports instantly, and allow management to access financial data from anywhere. Because of this sophistication, many business owners assume that once a cloud-based accounting system is implemented, financial stability is assured. However, system security and financial control are not the same thing.

In our consulting engagements, we repeatedly observe that financial disruptions rarely arise from system failure. They arise from internal actions—often unintentional—performed within the system itself. Bulk deletions, edits to historical transactions, or incorrect configuration changes can alter reports that management relies on for critical decisions.

The technology is functioning correctly. The governance framework around it may not be.

The Hidden Impact of Uncontrolled Changes

Consider what happens when entries in a closed period are modified without proper oversight. In systems that calculate inventory valuation using methods such as FIFO, a single historical edit can trigger a chain reaction. Cost of goods sold is recalculated, stock valuation shifts, profitability figures change, and previously reviewed reports no longer match.

This is not a technical malfunction. It is the natural consequence of dynamic accounting logic operating without controlled boundaries.

If financial statements can change without structured review and authorization, they are never truly final. When financial data lacks stability, decision-making becomes vulnerable. An accounting platform is not merely a data entry tool. It is a financial control framework. Without disciplined governance, automation can amplify risk rather than reduce it.

Three Essential Control Practices for Growing Businesses

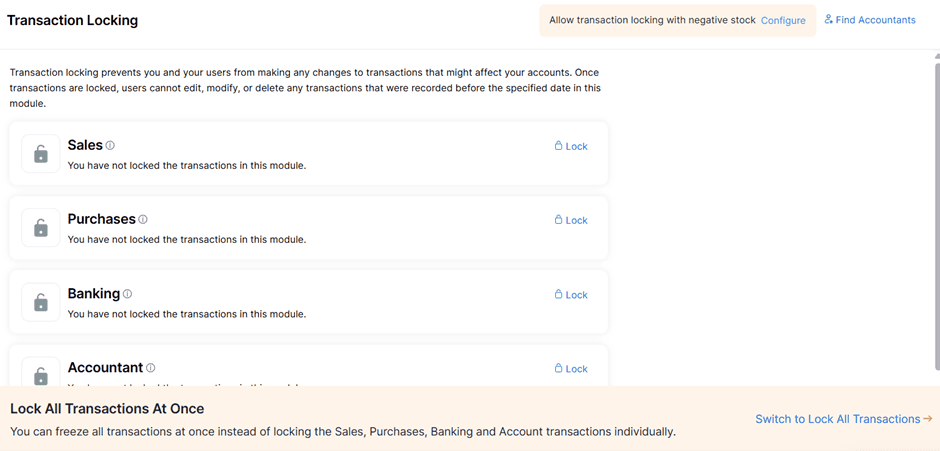

1. Periodic Locking of Closed Periods

Most modern accounting platforms provide the ability to lock transactions up to a specific date. For example, systems such as Zoho Books offer functionality to lock past-period transactions either module-wise or across the entire system.

This feature is not a technical convenience; it is a governance mechanism. A disciplined monthly closure process should include reconciliation, review, approval, and formal locking of the period. Overrides, when necessary, must follow defined authority protocols and be documented appropriately.

When this practice becomes routine, financial data gains stability and credibility.

2. Structured User Access Control

User access design is one of the most underestimated internal control mechanisms. In many growing businesses, system access is granted broadly for operational convenience. Over time, this creates exposure.

Every accounting system allows configuration of user roles and permissions. Access can typically be restricted by module, transaction type, approval rights, and edit authority. Yet these controls are often left at default settings or expanded without structured review.

Effective access control requires clarity on:

- Who can create transactions

- Who can edit transactions

- Who can delete entries

- Who can approve adjustments

- Who can unlock closed periods

Segregation of duties should be intentional, even in smaller teams. Where full segregation is not feasible, compensating controls such as management review, periodic audit log checks, and restricted override rights should be implemented. When authority mapping is unclear, accountability becomes diluted. A system with unrestricted edit rights is not a controlled environment; it is merely a digital ledger.

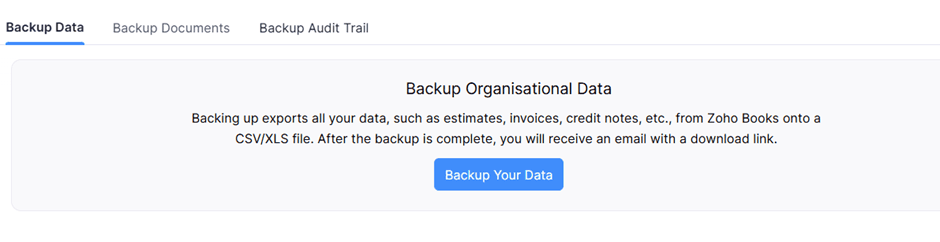

3. Scheduled Data Backups

Reputable cloud accounting platforms maintain high standards of infrastructure security and data reliability. However, internal resilience requires more than platform security.

Most systems provide options for periodic data backup or export.

Backups are not about questioning the safety of cloud hosting. They serve as point-in-time references that support audit verification, internal reconciliation, historical comparison, and recovery from human error. Regular backups create an additional layer of operational discipline. They ensure that if unintended edits occur, there is a reference baseline against which corrections can be evaluated.

Governance as a Strategic Advantage

As businesses scale, operational complexity increases. Financial systems begin to handle higher transaction volumes, multi-location inventory, integrated modules, and automated workflows. At this stage, informal practices become liabilities.

Strong digital governance includes:

- Defined monthly closure protocols

- Structured user role architecture

- Controlled override procedures

- Audit trail monitoring

- Periodic internal reviews of access rights

Technology provides capability. Governance ensures reliability. Without governance, automation increases exposure. With governance, automation strengthens control and builds institutional credibility.

A Leadership Responsibility

Internal financial controls are not merely the accountant’s responsibility. They are a leadership responsibility.

Business owners and management teams should periodically evaluate:

- Whether financial periods are formally closed and locked

- Whether user access rights reflect current roles and responsibilities

- Whether override permissions are restricted and documented

- Whether backups are taken and stored systematically

- Whether audit logs are reviewed as part of governance discipline

The objective is not restriction for its own sake. The objective is stability, accountability, and decision integrity.

Digital transformation is complete only when systems are supported by structured control architecture. Financial stability does not emerge from software features alone. It emerges from disciplined governance built around those features.

When control becomes institutional, confidence follows.